DEXTF Newsletter #20

Anniversary| DeFi Shots | DAMU L2 update | XTF2XXXSAD Fund breakdown | Coinbase, SEC, lending and low-interest rates: what's the nexus?

Hey Everyone,

Welcome to this week's edition of the DEXTF Newsletter!

Before getting started, here is a bit of celebration.

One year of democratizing access to asset management

As we celebrate our first anniversary today, we thank you all for the support through thick and thin. The whole DeFi ecosystem has evolved a lot in the last year and it feels great to be a part of it.

We look forward to keep on building to accomplish our mission of democratizing access to digital asset management.

You can follow the community conversations on Discord, Telegram, Twitter, and Reddit!

DEXTF updates

We launched DeFi Shots, our DeFi curation arm. This will be a weekly feature capturing the best of #DeFi and our analysis of it. Exclusively on DAMU (damu.dextf.com).

As a part of the staggered release, we made the first article on L2 module live.

Here is this week’s fund breakdown (XTF2XXXSAD) launched on DEXTF.

Note the “XTF2” which means that it’s a v2 fund token!

For those that want to dig into what’s DEXTF, this is a good start:

Also, DEXTF is hiring! If you think this is you, reach out to us. DMs are open.

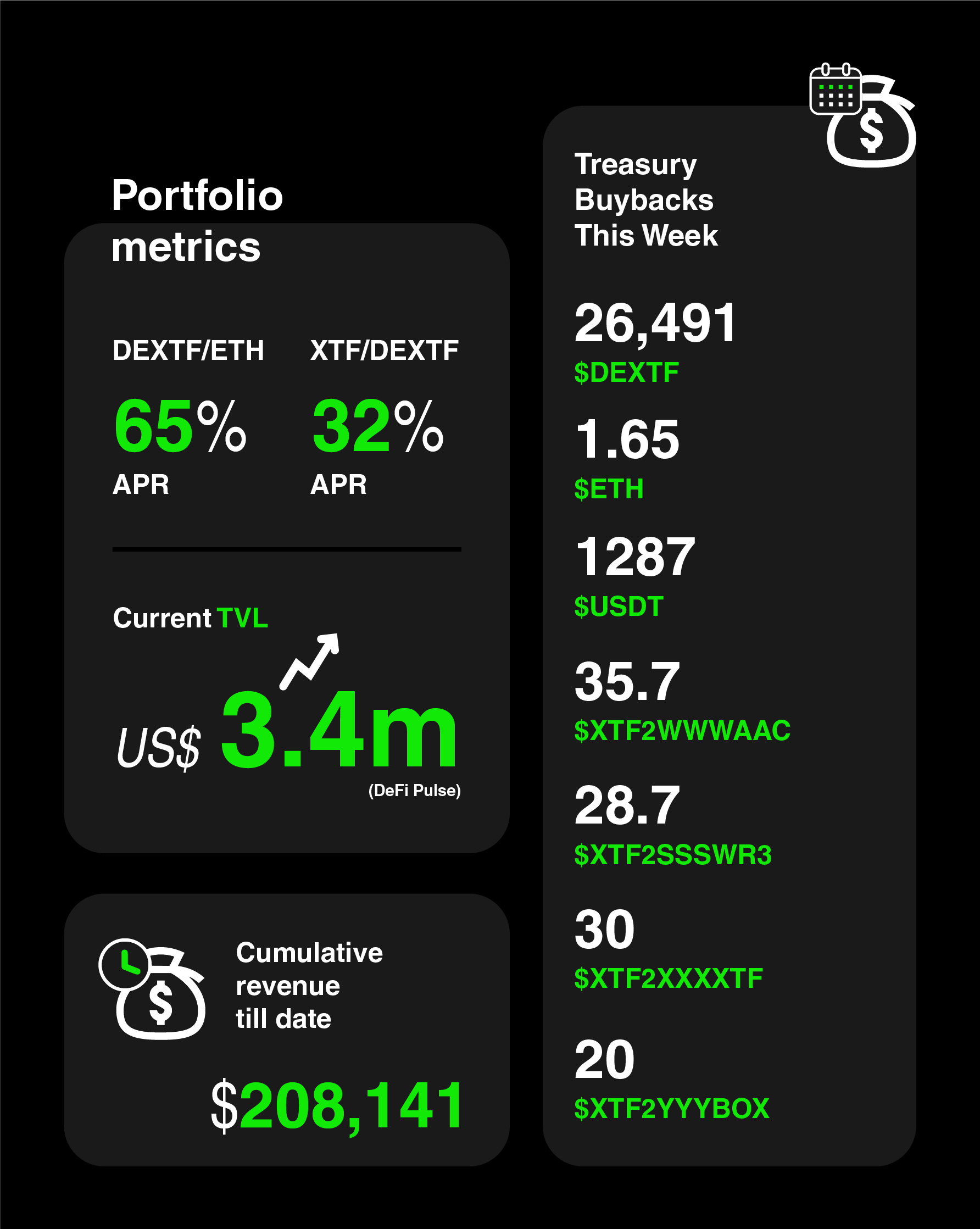

Portfolio Metrics

Please refer to the DEXTF website for the latest APRs:

DEXTF/ETH is offering a 65% APR

XTF/DEXTF is offering a 32% APR

You can also earn $DEXTF by providing liquidity on Uniswap (29.6K tokens daily) or investing in any of the XTF funds (12K tokens daily)

Current TVL is US$3,400,000

You can invest by buying on Uniswap or on the DEXTF app

Here’s a quick guide on how to buy

Protocol Revenue

DEXTF has a cumulative treasury revenue of US$208,141.67 since the Treasury started.

Over the course of this week, the treasury accumulated these Assets:

26,491 DEXTF

1.65 ETH

1287 USDT

35.7 XTF2WWWAAC

28.7 XTF2SSSWR3

30 XTF2XXXXTF

20 XTF2YYYBOX

Concept of the Week

⚖️ Coinbase, SEC, lending and low-interest rates: what's the nexus?

Before we begin our analysis on the developing Coinbase vs. SEC case, here is a tweet by Brian Armstrong, CEO of Coinbase, summarising the situation:

A regulatory crackdown by the SEC this year on crypto unicorn darlings was probably expected. This is not surprising as regulators' job is to seek clarification through ambiguous guidance or statements around a controversial product. But when it comes to investor protection, Gary Gensler - the widely celebrated 33rd SEC chairman who was supposed to be crypto-friendly -does not make exceptions. He is, in fact, a technology-neutral.

So what exactly did Coinbase do to get sued by the SEC?

Like all successful businesses, diversification of services increases stickiness which leads to increased revenue and brand loyalty. Coinbase, a centralized crypto exchange, has made its name by efficiently carrying out trades for retail and professional traders without data breaches.

Coinbase provides besides token exchange services also:

payment software and support to online retailers to facilitate crypto payments

Visa debit card issuer, enabling easy and real-time crypto spending in the physical world

Coinbase Lend is a new service that pays a guaranteed 4% APY (compounded interest) on USDC deposits. USDC is a crypto stablecoin pegged 1:1 to the US dollar.

So here are where the problems begin.

To give some perspective, Coinbase's total net income up to 2021 Q2 is ~ US$ 2.3 billion, which is already 3.7x the net income reported by Deutsche Bank for the entire year of 2020. And assuming the same performance over the second half of the year, the firm could be pulling in ~US$ 4.6 billion, which is 0.5x the net income of Goldman Sachs over 2020.

In short, by launching this product, Coinbase is signaling that it wants to become a bank that pays its depositors over 8x the interest paid on average in the US, as stated on their website (https://www.coinbase.com/lend). And if it wasn't clear enough, Coinbase guarantees that yield.

Financial institutions have been quite skeptical of the crypto industry, but many have turned around to support it as demand was simply unstoppable. Nevertheless, that does not mean they are embracing it. Crypto, particularly DeFi, hinges on the narrative of disintermediating the middleman, represented today by banks, custodians, asset managers, etc. However, DeFi, despite growing its Total Value Locked to ~ US$90 billion, still can't provide valuable, cheap, and easy access to crypto to the vast retail and institutional investors. It needs a centralized entity to bridge TradFi to DeFi or, in general, to crypto.

To understand the issue, let's dig deeper into what a product like Coinbase Lend does to the banks' deposit profit margin.

On Aug 23, 2021, the Federal Reserve Bank of San Francisco published an evocative Economic Letter; a negative interest rate environment can negatively impact banks' net interest margins (profit derived from spread between FED policy rates and deposit rate). The FED policy rates affect asset valuations and are used to regulate the economy (and inflation).

The paper argues that banks can't pay negative rates to depositors even if the policy rates go below zero. That's intuitive because the cost of keeping your cash at home is really minimal, so if you need to pay to deposit, a great majority, if not all, would rather keep the cash under their mattresses.

Established that, the paper continues and says that although banks can still churn out a profit because of the interest earned from the higher bank loan rate, this decreases steeply when the policy rate is negative.

Therefore, it is assumed that banks would rather not accept any deposit to stop the bleeding at a certain point. Although this situation has not happened yet as the negative policy rates should reach -2% according to the study, a much higher deposit rate offered by Coinbase Lend greatly hinders the pricing power and, in turn, the purpose of the central bank's policy rate.

To conclude, the size at which Coinbase has grown together with its track record might pose a threat to financial institutions and, with it, the central bank's wiggling space.

Semper Fortis

DEXTF Team