DEXTF Newsletter #18

New DeFi Jabs Episode | Extention in deadline for applying to Centurion Program | What is market making?

Hey Everyone,

Welcome to this week's edition of the DEXTF Newsletter!

You can follow the community conversations on Discord, Telegram, Twitter, and Reddit!

DEXTF updates

The second episode of the DeFi jabs podcast is now live!

We are extending the deadline to apply for the DEXTF Centurion program!

We are extending the deadline to apply for the DEXTF Centurion program! You can now apply till 30 August 11:00 AM UTC. If you still haven't, apply here: forms.gle/xqPHFDt9vrMv3D…DEXTF democratizes asset management, tokenizing one portfolio at a time. While doing this, we want to grow a passionate community that will magnify DEXTF’s vision. As a result, we are excited to announce DEXTF’s Centurion (Ambassador) Program! 1/5 https://t.co/0gxAqSttpK

We are extending the deadline to apply for the DEXTF Centurion program! You can now apply till 30 August 11:00 AM UTC. If you still haven't, apply here: forms.gle/xqPHFDt9vrMv3D…DEXTF democratizes asset management, tokenizing one portfolio at a time. While doing this, we want to grow a passionate community that will magnify DEXTF’s vision. As a result, we are excited to announce DEXTF’s Centurion (Ambassador) Program! 1/5 https://t.co/0gxAqSttpK DEXTF Protocol @dextfprotocol

DEXTF Protocol @dextfprotocol

For those that want to dig into what’s DEXTF, this is a good start:

Also, DEXTF is hiring! If you think this is you, reach out to us. DMs are open.

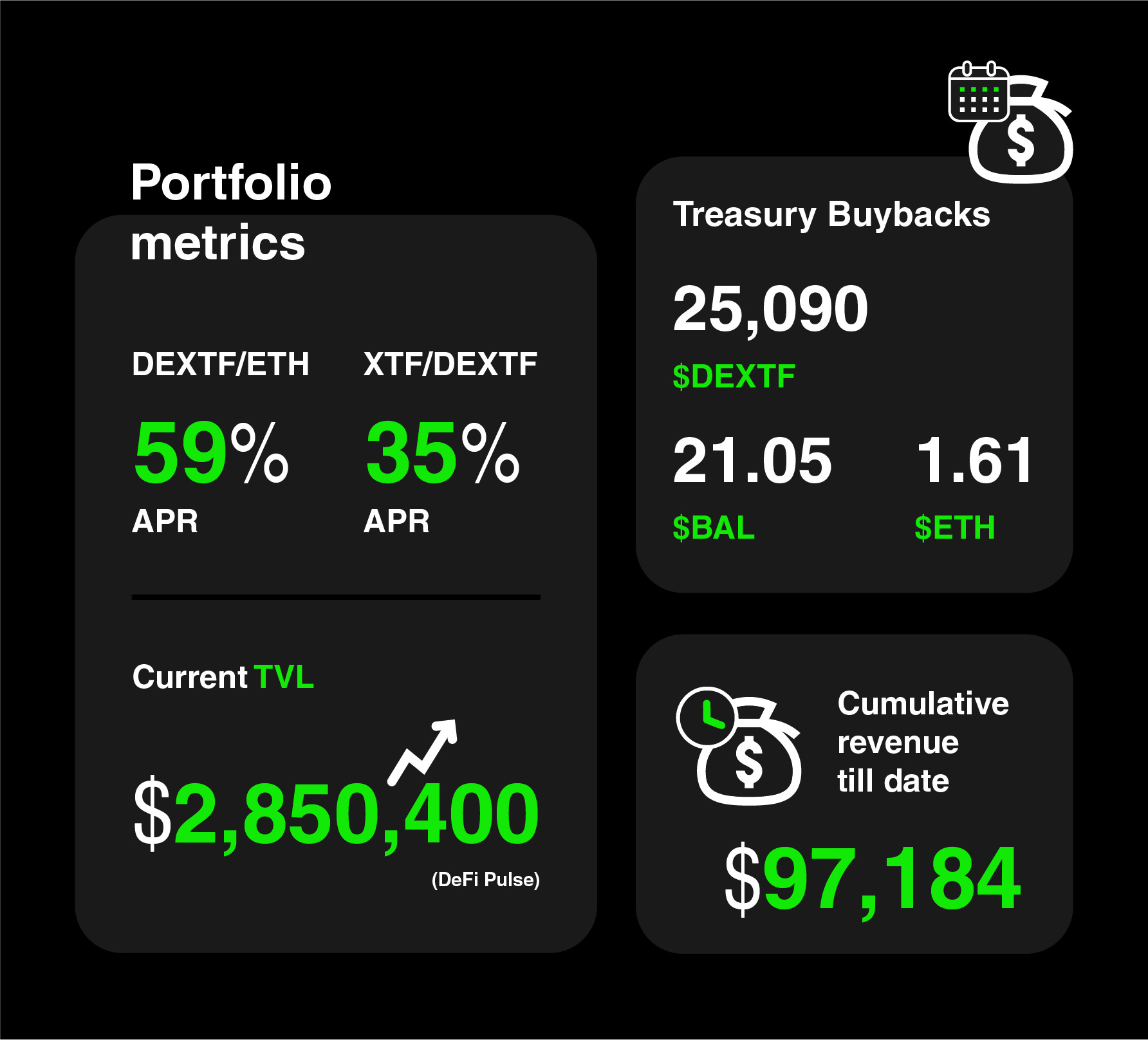

Portfolio Metrics

[As of 26th August 2021].

Please refer to the DEXTF website for the latest APRs:

DEXTF/ETH is offering a 59% APR

XTF/DEXTF is offering a 35% APR

You can also earn $DEXTF by providing liquidity on Uniswap (29.6K tokens daily) or investing in any of the XTF funds (12K tokens daily)

Current TVL is US$2,850,400

You can invest by buying on Uniswap or on the DEXTF app

Here’s a quick guide on how to buy

Protocol Revenue

DEXTF has earned cumulatively US$$97,184K in revenue since the Treasury started

To date, the cumulative amount of assets bought back by the Treasury are:

25090 $DEXTF

21.05 $BAL

1.61 $ETH

Concept of the Week

⚖️ What is market making?

Market makers are centralized or decentralized liquidity providers optimizing for trade slippage. As a result of the activity of market makers, traders can buy and sell any tradables with ease knowing that there's sufficient liquidity to accommodate the trade without a sizable price impact.

Market making in TradFi

Market making is a line of business that involves huge working capital and inventory risk that in TradFi only big financial institutions or specialized firms are able to manage. Though, that's not the only reason why all in all it isn't such a crowded space. Regulatory constraints play an active role in shaping this industry.

For instance, market makers (MM) in certain jurisdictions could be subject to an obligation to provide 50% of the liquidity for each trading day. But then, would be exempted in case of extreme market turbulence caused by unexpected real-world events such as an act of war, or simply during a very volatile period.

Volatility is probably traders' best friend. And not being able to interact with it means more chaos and less efficient markets, which is what the market maker is supposed to guarantee.

Despite the "limited" number of competitors, market makers would go to great strides to eke out an edge versus the others. Receiving price feeds at lightning speed or at a few milliseconds quicker than the others can literally make or break a market making strategy, as in the case of HFTs (High Frequency Traders). MM’s datacenters co-located next to exchange servers would do the trick (the cost of setting it up is not small).

Market Makers in DeFi

If TradFi enlists centralized entities to market make, DeFi democratizes liquidity providing through code. Traders would therefore interact with liquidity pools governed by smart contracts.

Suddenly data centers' proximity to data feeds becomes irrelevant. Although all transactions are recorded in the blockchain, where and how value flows across the protocols and AMMs became the treasure trove. The emergence of analytics providers such as Nansen, Skew, Chainanalysis, Dune Analytics is evidence that fundamental analysis has become less predictive and more multidimensional.

DeFi is the crib to Automated Market Makers or AMMs. Uniswap is one of the very first decentralized exchanges that allow the creation of new markets for token pairs and for anyone to provide liquidity. Kyber Network is known to be the first DEX, but liquidity provision wasn't open to the public.

This meant that many projects didn't have to pay centralized exchanges the hefty listing fees, solving immediately and inexpensively the most obvious chicken-and-egg problem.

No liquidity token projects lead to less adoption, which means that projects can never deliver what they promised to deliver. With AMMs, any retail investor could decide to supply their tokens to become liquidity providers, effectively socializing profit and losses in the difficult business of market making for long-tail assets.

Long-tail assets in AMMs are those assets that centralized market makers have no edge upon, as the predictability of short-term asset movements is too volatile for them to provide their services and earn a spread. Liquidity providing as a retail investor in a 50/50 pool however is not the most efficient in terms of working capital, especially if you consider the potential "impermanent loss" that each LP is going to face when volatility increases.

Hence, similarly to TradFi, trading rebates are awarded to liquidity providers given their length of stay in the pool, in what it is known today as liquidity mining rewards, often distributed in the native token.

The existence of LPs in AMMs however does not prevent centralized MMs to do what they've always been good at. Buying low and sell high simultaneously. Now, this can be done between centralized exchanges and decentralized exchanges, where the blockchain execution lag and different kinds of bot activities created an interesting arbitrage environment.

Decentralized customization is the future

AMM aggregators have become so efficient today that they can offer solutions that combine the best of decentralized exchanges and centralized market makers. This is the case of the 0x RFQ system, where market makers could even select their potential counterparty, eliminating the risk of being abused.

AMM disadvantages

price impact (slippage)

sandwich attacks (a specific case of front-running)

deterministic pricing

liquidity providers make a loss when volatility picks up (external incentive reliant)

Conclusion

In summary, the disadvantages while addressable would greatly prevent interest from rising without further innovation by aggregating AMMs with centralized entities that push bid-ask in competition to AMMs. The user would then get the best universal quote.

Semper Fortis

DEXTF Team