DEXTF Newsletter #10

Rewards simplified? Protocol Treasury executed buyback of 70,383 $DEXTF, and crypto assets valuation ep.1

Hey Everyone,

Welcome to this week's edition of the DEXTF Newsletter!

You can follow the community conversations on Discord, Telegram, Twitter, and Reddit!

DEXTF updates

For those that want to dig into what’s DEXTF, this is a good start:

A community request to simplify the liquidity mining rewards was put to vote:

How to create a fund (and launch it) in one step!

Also, DEXTF is hiring! If you think this is you, reach out to us. DMs are open.

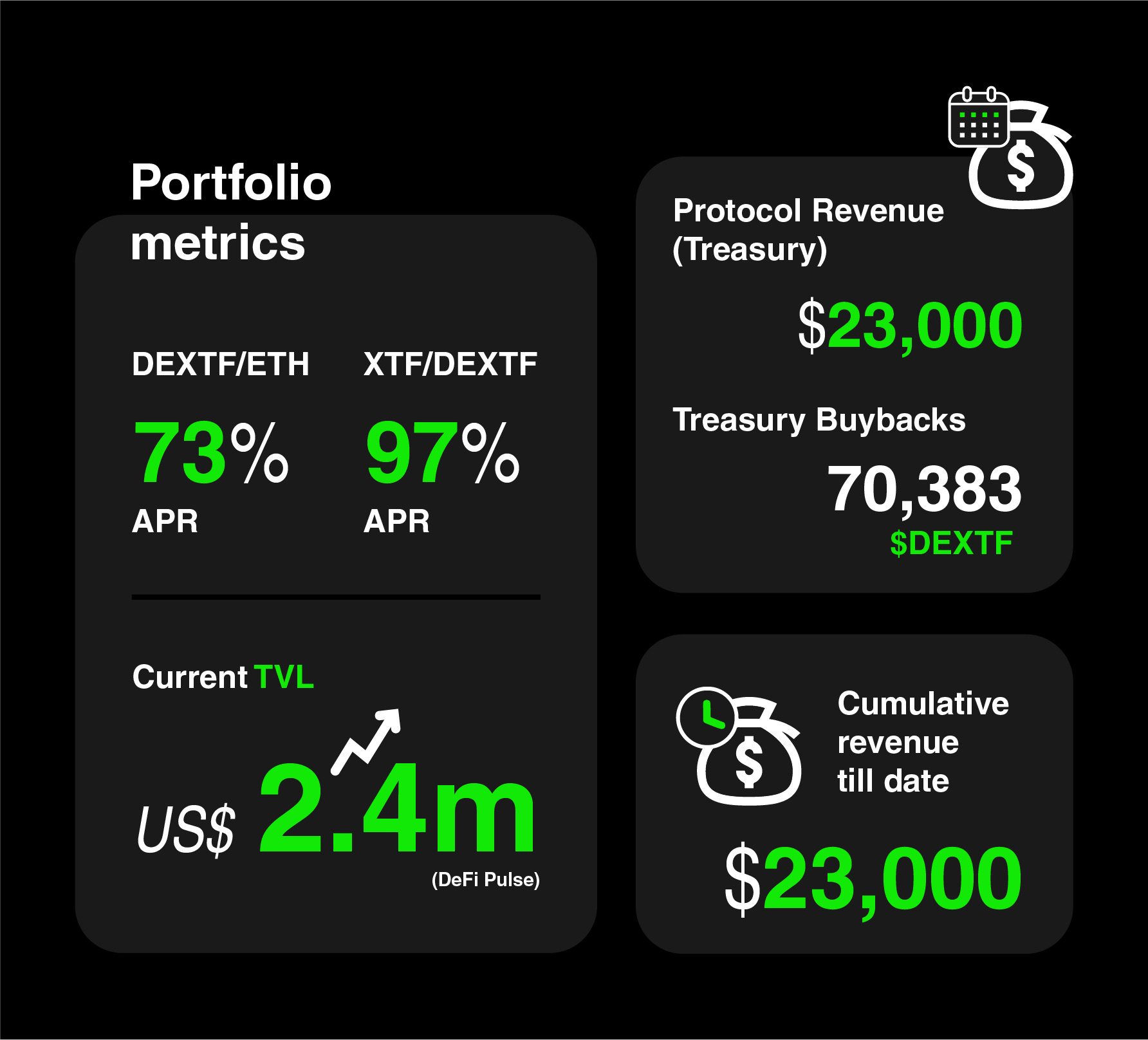

Portfolio Metrics

[As of 1st Jul 2021].

Please refer to the DEXTF website for the latest APYs:

DEXTF/ETH is offering 73% APY

XTF/DEXTF is offering 97% APY

You can also earn $DEXTF by providing liquidity on Uniswap (29.6K tokens daily) or investing in any of the XTF funds (12K tokens daily)

Current TVL is US$ 2.4M (refer to DeFi Pulse)

You can invest by buying on Uniswap or on the DEXTF app

Here’s a quick guide on how to buy

Protocol Revenue

Since DIP-4 has passed, a Protocol Treasury was established with the objective of generating revenue used to, among other things, buyback $DEXTF for distribution to stakers.

We’re excited to share that the Treasury has started to allocate its resources in the past week and has completed a buyback of 70,383 $DEXTF.

Concept of the Week

⚖️ Crypto assets valuation pt. 1

When it comes to valuing crypto assets, there’s no one metric that can be reliably called up every time by anyone.

As all novel assets, a speculative frenzy in 2017 has attracted a great amount of capital from VCs and retail mom-and-pops. What’s often ignored is that this pump-and-dump has laid the grounds for a slew of projects that today are minting cash flowing towards token holders.

Suddenly, concepts that in TradFi are generally taken for granted start to apply also for crypto.

Let’s go through some of these concepts.

Present Value and Future Value

Interest rates

Value is inextricably linked to interest rates.

Interest rates are a very simple concept yet very often it’s easy to get confused by it.

Through this write-up, we attempt to shed some clarity on this topic.

When we talk about present value (PV) or future value (FV), we assume that time is money, hence in finance, we refer to time value.

Time is valued through the interest rate. In particular:

If you want to know what is the value of a future asset in today’s terms, you use a discounting rate (Present Value)

When assessing risk in investable assets, we refer to rate of return, which represents the return that would be required to satisfy investors for lending out their funds to the market

Interest rates can be interpreted as opportunity costs.

Oftentimes, traders end up comparing different farms versus hodling. Comparing rate of returns from hodling and APRs/APYs for farming, it’s effectively making an opportunity cost analysis. Usually, it’s the answer to if I jump into this opportunity, what will I be missing had I considered the alternative?

Lastly, interest rates can be nominal (on paper) or real (when inflation is considered).

Nominal interest rates could be positive when in reality that same return would not be buying the same basket of goods (let’s simplify it as a basket of bread) that you previously could.

Inflation simply means a decrease in the value of money. If the value of money decreases, you get in return fewer goods. It is the ultimate exchange rate that you need to perform when holding a base currency.

For every market, there’s a real risk-free rate (RRFR), which is used in valuation models.

The RRFR is a benchmark on which all other returns are based. It can be understood as the last resort return that you can receive with virtually no risk, hence it’s also the lowest rate in that market.

Semper Fortis

DEXTF Team